How do you react when your phone vibrates or the notification light blinks in your pocket? Regardless of what you are doing at that moment, your hand likely reaches for the device instinctively. This is the conditioned reflex of the modern age. This "impulse to check," explained by the dopamine loop, harbors immense, untapped potential for the financial world.

Traditional financial content often focuses on dry statistics; however, the secret behind the success of Pay-by-Link technology is not just that it is a financial tool, but that it transforms this powerful human psychology into a "growth" strategy. Your customer might see an email days later—or perhaps never at all. However, they will read an SMS notification arriving on their mobile phone within an average of 90 seconds.

When businesses utilize this golden 90-second window correctly, they can turn cash flow crises into opportunities. In this guide, we explore how Pay-by-Link systems accelerate collection processes by 40% or more, analyzed through the lens of data-driven evidence and financial engineering.

What is Pay-by-Link?

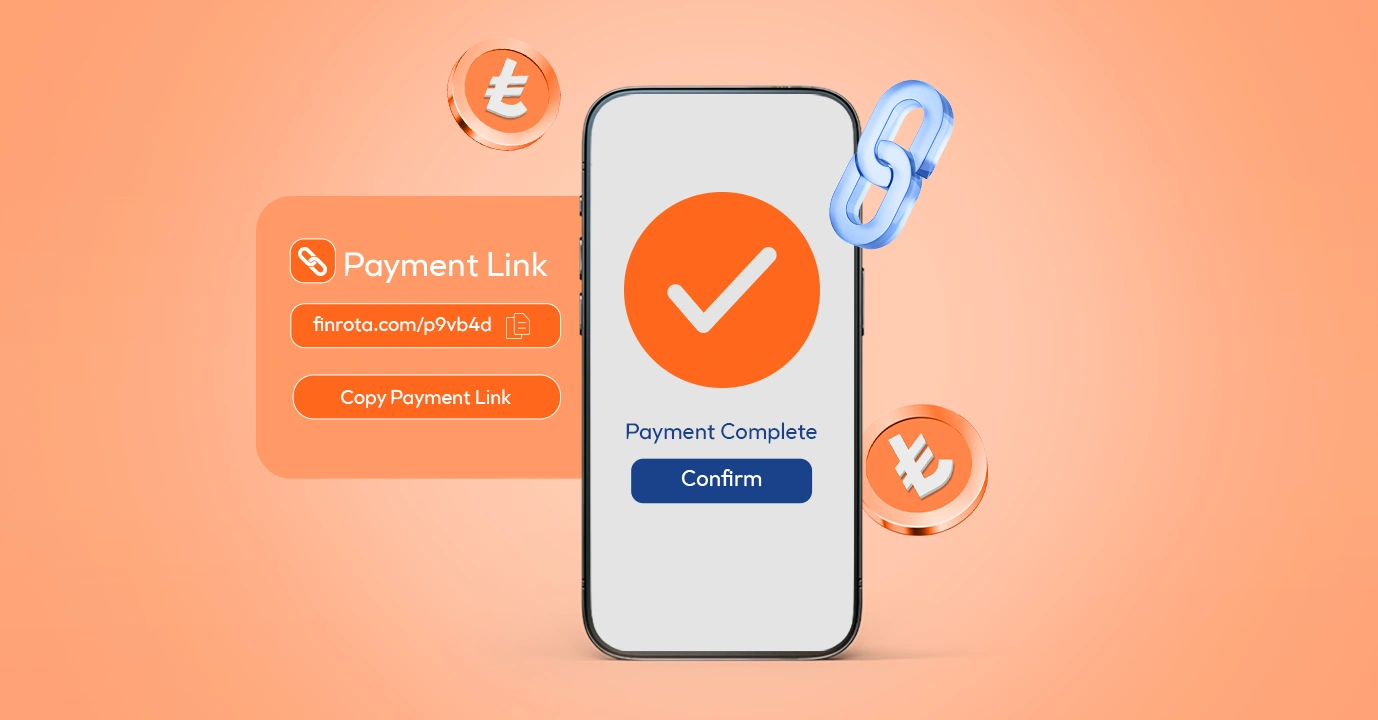

Pay-by-Link is a financial technology that enables businesses to collect payments via credit card through a virtual POS infrastructure by sending a secure payment URL to customers via SMS, Email, or WhatsApp.

The process operates through the following steps:

Initiation: The merchant or the integrated ERP system determines the payment amount.

Generation: The system generates a unique and secure payment link.

Transmission: The link is delivered to the customer via their preferred communication channel (specifically SMS).

Action: The customer clicks the link, enters card details, and confirms the transaction via 3D Secure.

Reconciliation: The payment result is instantly processed into the accounting system.

The Operational Deadlocks of Traditional Methods

For modern commercial enterprises, "time" is a direct cost. In inflationary environments, every day a payment remains uncollected creates an erosion in the real value of money. Traditional methods, however, struggle to keep pace with the speed of the digital age.

The Burden of Bank Transfers/EFT: Requiring a customer to log in to a banking app, copy an IBAN, and manually enter the amount and description creates significant "friction." Research indicates that this hassle causes customers to postpone payment to a "more convenient time." Furthermore, errors stemming from manual data entry can lead to funds remaining in limbo.

Mail Order Insecurity: The Mail Order system, where card details are taken over the phone, is no longer sustainable regarding GDPR (KVKK) and data security standards (PCI-DSS). Customers are rightfully reluctant to share card details verbally.

Pay-by-Link technology shifts the process from a "waiting" axis to an "interaction" axis. When the customer clicks the link, the amount, recipient, and description are already populated. All they need to do is confirm the payment.

The Power of Communication Channels: Why SMS and Not Email?

The claim of shortening collection times is rooted not just in the speed of the payment infrastructure, but in the "speed of communication." For a payment to be made, the customer must first be aware of the debt and then take action. This is where the performance chasm between SMS and Email becomes decisive.

1. Open Rates Statistics show that email marketing has reached a point of saturation.

Email: Average open rates hover in the 20-32% range. Approximately 70 out of every 100 reminders sent are never read.

SMS: The open rate for text messages is at the 98% level. Almost every notification sent is seen by the recipient.

2. Response Time and the Speed Factor The most critical metric affecting collection speed is the time between message delivery and the moment it is read.

The average read time for an email can reach 90 minutes.

An SMS is read, on average, within 90 seconds of delivery.

This 90-second reaction time is vital, especially for past-due or urgent payments. The moment the customer sees the notification, they are inclined to complete the payment through a behavioral "nudge."

Financial Impact: DSO and Cash Flow Management

For CFOs and business owners, Pay-by-Link is more than a simple convenience; it is a strategic tool that improves financial statements. The most distinct impact is observed in the DSO (Days Sales Outstanding) metric.

Pay-by-Link systems drive down DSO by minimizing the time spent on invoice transmission and payment action. It is reported that companies switching to digital collection solutions and automating the process achieve an improvement of 40% or more in collection times.

A decrease in DSO means the following for your business:

Reduced Need for Credit: Since the business converts its own receivables into cash faster, the need for bank loans and interest costs decreases.

Investment Capability: Cash surplus can be directed towards growth opportunities or used to secure cash payment discounts on raw material purchases.

Eliminating Operational Load: ERP Integration

For the increase in collection speed to be sustainable, the process must become independent of human intervention. Modern payment platforms like Finrota and Paynet work with two-way integration with common ERP software such as SAP, Logo, Mikro, and Netsis.

Invoice -> Link: The moment an invoice is generated in the ERP, the system automatically creates an SMS link and transmits it to the customer.

Payment -> Receipt: When the customer pays via the link, the system instantly writes this information back to the ERP and deducts it from the current account balance.

This automation reduces errors caused by manual data entry to zero and saves hours that the accounting department would otherwise spend reconciling "who sent this money."

Perception of Security: PCI-DSS and 3D Secure

While speed is important, security is paramount in financial transactions. Asking customers to click on an unknown link and enter card details is an action requiring trust.

Professional Pay-by-Link infrastructures possess PCI-DSS (Payment Card Industry Data Security Standard) certification. This guarantees that card data is encrypted according to international standards. Furthermore, processing transactions with 3D Secure protects the merchant against "Chargeback" risks while reassuring the customer with an SMS code from their bank. The customer knows they are entering their details on a secure banking screen, not sharing them directly with the merchant.

Frequently Asked Questions

Is Pay-by-Link secure? Yes, professional Pay-by-Link systems adhere to PCI-DSS security standards, and transactions are verified via 3D Secure. Card information is not shared with the merchant; it is processed in an encrypted manner directly within the banking infrastructure.

Does the customer need to download an app? No, Pay-by-Link works on a browser basis. The customer does not need to download any application, create a membership, or fill out complex forms. Clicking the link is sufficient.

Through which channels can the payment link be sent? Payment links can be shared primarily via SMS, but also through Email, WhatsApp, or other social media channels. In B2B collections, sharing links and invoices via WhatsApp is quite common.

Does the system integrate with accounting software? Yes, most advanced payment systems work in integration with widespread ERP and accounting programs like SAP, Logo, Mikro, Netsis, and DİA, automatically reconciling payments.

Digital Transformation in Collections

"Pay-by-Link" technology, the reflection of digital transformation in financial operations, is no longer a luxury for modern businesses but an operational necessity. By combining communication speed (98% SMS read rate), transaction ease (one-click payment), and operational efficiency (automated accounting), these systems secure cash flow.

Digitizing your collection processes to escape the time costs created by traditional habits and to protect your financial health will be one of the most profitable steps you can take.